AGU Publications

2002

Tectonic evolution of the Principal Cordillera

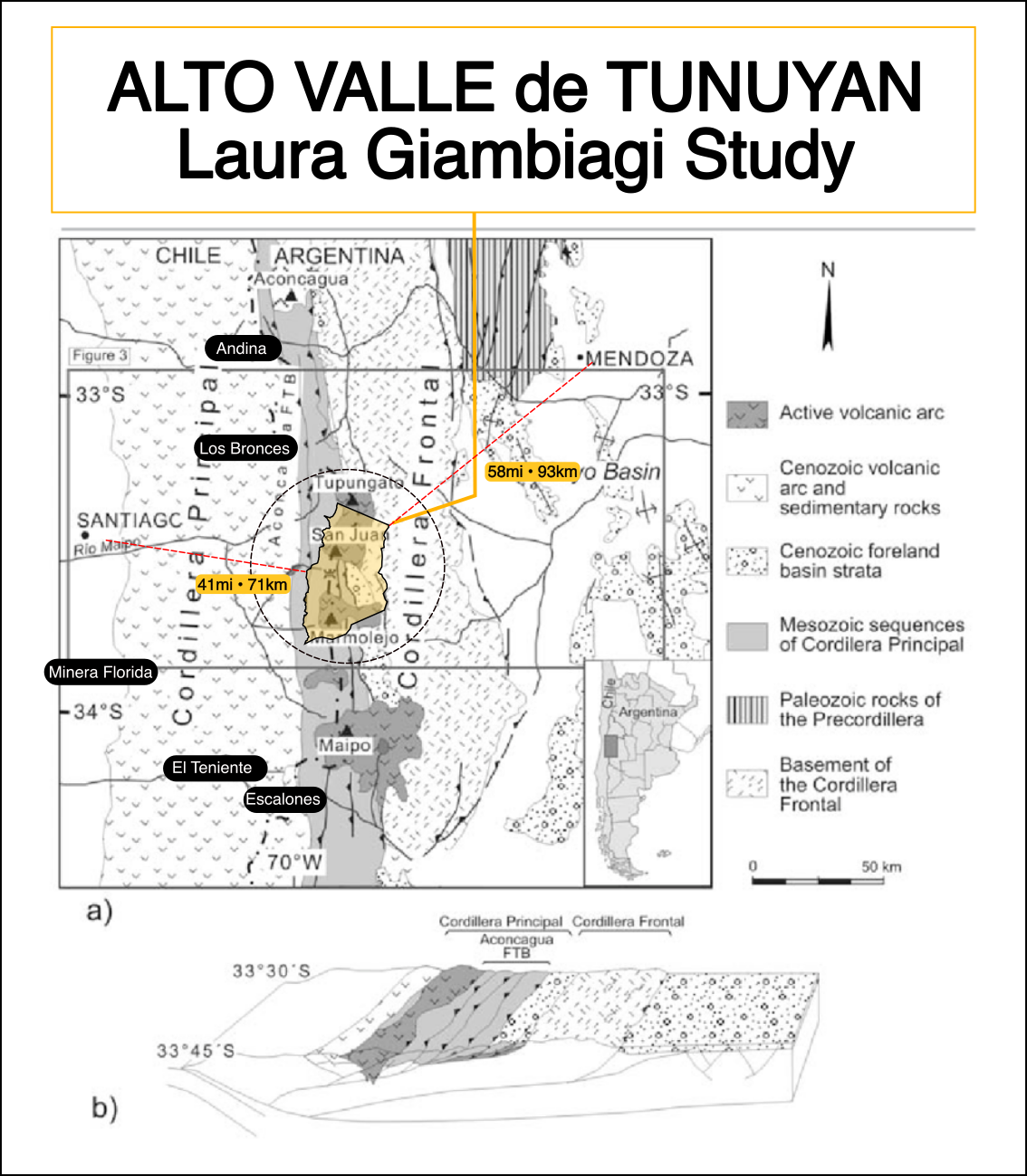

Evolución tectónica de la Cordillera Principal a 33°–34°S, zona del Alto Tunuyán.

Glaciares The Guardian

Argentina acaba de derogar su pionera ley de glaciares, poniendo en riesgo las reservas de agua de millones

10 abr 2026

Glaciares The Guardian

Argentina acaba de derogar su pionera ley de glaciares, poniendo en riesgo las reservas de agua de millones

10 abr 2026

Vicuña Los Andes

San Juan encuentra el Vaca Muerta del cobre con niveles de pureza excepcionales

10 abr 2026

Vicuña Los Andes

San Juan encuentra el Vaca Muerta del cobre con niveles de pureza excepcionales

10 abr 2026

Chile Los Andes

Roberto Cacciola en Mendoza: ahora tienen que aparecer los proyectos mineros

Abr 2026

Chile Los Andes

Roberto Cacciola en Mendoza: ahora tienen que aparecer los proyectos mineros

Abr 2026

Mendoza Los Andes

La Declaración de Impacto Ambiental Don Luis avanza en San Rafael y Malargüe

Abr 2026

Mendoza Los Andes

La Declaración de Impacto Ambiental Don Luis avanza en San Rafael y Malargüe

Abr 2026

Chile Los Andes

Jimena Latorre: la minería puede ser el vector de crecimiento de América Latina

Abr 2026

Chile Los Andes

Jimena Latorre: la minería puede ser el vector de crecimiento de América Latina

Abr 2026

Los Azules Los Andes

Los Azules puede convertirse en un polo clave de cobre a nivel global

Abr 2026

Los Azules Los Andes

Los Azules puede convertirse en un polo clave de cobre a nivel global

Abr 2026

Mendoza Sitio Andino

Minería en Mendoza: empresas se preparan el despegue del sector

Abr 2026

Mendoza Sitio Andino

Minería en Mendoza: empresas se preparan el despegue del sector

Abr 2026

Las Heras Los Andes

Los Andes en Canadá: Mendoza avanza con un distrito minero en Las Heras

Mar 2026

Las Heras Los Andes

Los Andes en Canadá: Mendoza avanza con un distrito minero en Las Heras

Mar 2026

Canadá Los Andes

Los Andes en Canadá: Hebe Casado dijo que ha sido una feria muy productiva para Mendoza

Mar 2026

Canadá Los Andes

Los Andes en Canadá: Hebe Casado dijo que ha sido una feria muy productiva para Mendoza

Mar 2026

Canadá Los Andes

Los Andes en Canadá: la minería es la madre de las industrias, dijo Latorre al presentar a Mendoza ante inversores

Mar 2026

Canadá Los Andes

Los Andes en Canadá: la minería es la madre de las industrias, dijo Latorre al presentar a Mendoza ante inversores

Mar 2026

Mendoza Exploración

Minería: Mendoza en el ojo de los inversores para avanzar en tareas de exploración

Mar 2026

Mendoza Exploración

Minería: Mendoza en el ojo de los inversores para avanzar en tareas de exploración

Mar 2026

Vicuña El Economista MX

Vicuña Corp anuncia inversión récord de USD 18.000 millones en Argentina

16 feb 2026

Vicuña El Economista MX

Vicuña Corp anuncia inversión récord de USD 18.000 millones en Argentina

16 feb 2026

Vicuña Los Andes

Milei recibe al CEO de Vicuña con inversión récord de USD 18.000 millones

Feb 2026

Vicuña Los Andes

Milei recibe al CEO de Vicuña con inversión récord de USD 18.000 millones

Feb 2026

Canadá Entrevista

Stewart Wheeler: El interés de las empresas canadienses por Argentina sigue creciendo

Feb 2026

Canadá Entrevista

Stewart Wheeler: El interés de las empresas canadienses por Argentina sigue creciendo

Feb 2026

Argentina Inversiones

El potencial de la minería en Argentina: proyectan inversiones por u$s63.700 millones y exportaciones que podrían quintuplicarse hacia 2035

Feb 2026

Argentina Inversiones

El potencial de la minería en Argentina: proyectan inversiones por u$s63.700 millones y exportaciones que podrían quintuplicarse hacia 2035

Feb 2026

Glaciares Global News

Corte argentina niega a Barrick la medida cautelar contra la ley de glaciares

Ene 2026

Glaciares Global News

Corte argentina niega a Barrick la medida cautelar contra la ley de glaciares

Ene 2026

Glaciares BA Herald

Milei presenta proyecto para modificar la ley de glaciares y favorecer la minería

Dic 2025

Glaciares BA Herald

Milei presenta proyecto para modificar la ley de glaciares y favorecer la minería

Dic 2025

RIGI + Vicuña Lundin

Vicuña Corp aplica al RIGI para proyecto PEELP en Argentina

Nov 2025

RIGI + Vicuña Lundin

Vicuña Corp aplica al RIGI para proyecto PEELP en Argentina

Nov 2025

RIGI Cancillería

Guía para inversores: Régimen de Incentivo a Grandes Inversiones (RIGI)

Oct 2025

RIGI Cancillería

Guía para inversores: Régimen de Incentivo a Grandes Inversiones (RIGI)

Oct 2025

Mendoza Sitio Andino

Cornejo presenta en Londres oportunidades de minería, energía y petróleo

Sep 2025

Mendoza Sitio Andino

Cornejo presenta en Londres oportunidades de minería, energía y petróleo

Sep 2025

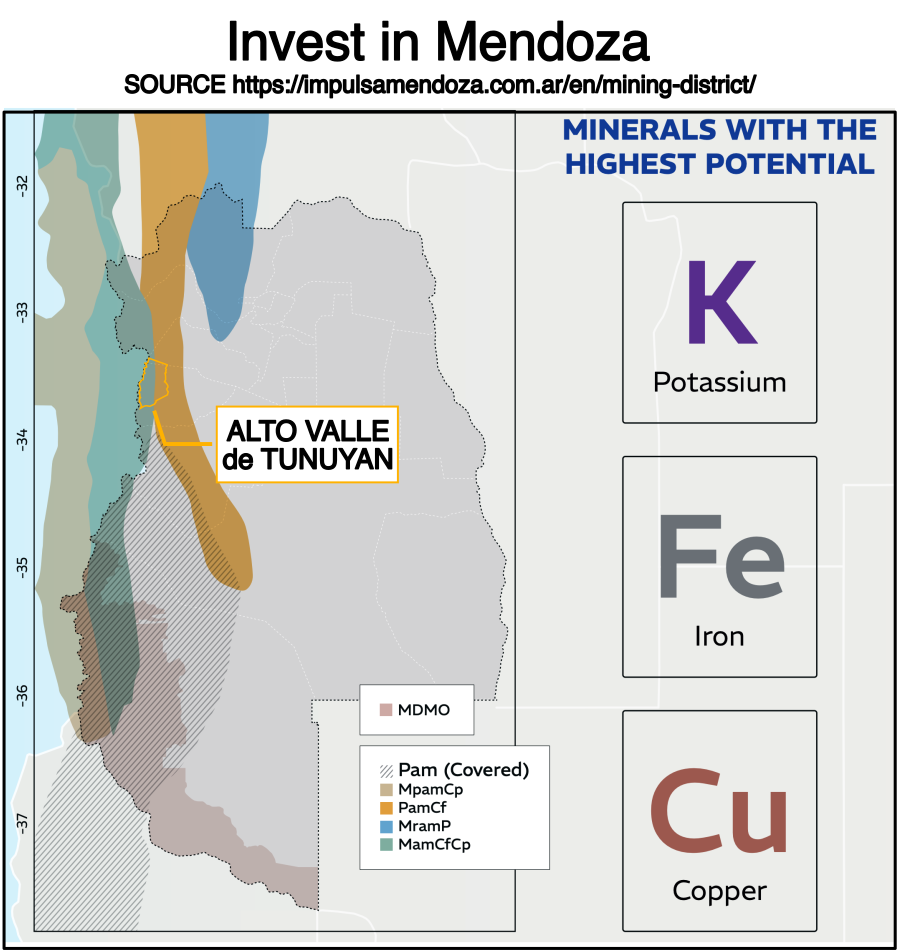

La propiedad ocupa una posición territorial continua entre Mendoza y la frontera chilena, en el Paso Piuquenes.

La geografía es permanente. La ubicación define el potencial de desarrollo de recursos a largo plazo.

Alto Valle de Tunuyán posee una DOBLE Ventaja Estratégica: se encuentra dentro del Cinturón Cuprífero Andino en la misma latitud que El Teniente y Los Bronces — y, al mismo tiempo, se ubica sobre el eje logístico transandino histórico más corto entre Buenos Aires, Mendoza y Santiago, activo desde el siglo XVII.

La propiedad se sitúa directamente sobre el corredor colonial que conectó Buenos Aires, Mendoza y Santiago a través del Paso Piuquenes y el Paso del Portillo. Este eje precede a la infraestructura moderna, pero sigue representando el cruce estructural más directo entre ambas capitales.

En minería, la geología define el potencial — pero la LOGÍSTICA define la viabilidad. A solo 93 km de Mendoza y 71 km de Santiago, el activo combina continuidad mineral con acceso binacional estratégico.

Continuidad geológica y continuidad logística. Dotación mineral y acceso estructural. Potencial de recursos y poder de corredor.

Las áreas de proyecto se ubican dentro del Cinturón Cuprífero Andino, mostrando continuidad estructural con los principales depósitos cupríferos chilenos en la misma latitud.

El contexto geológico indica un entorno estructural favorable. No se ha realizado perforación. Se requiere verificación técnica.

Estudios académicos y técnicos que fundamentan el potencial minero de la región

Evolución tectónica de la Cordillera Principal a 33°–34°S, zona del Alto Tunuyán.

Estudio de procedencia de la Cuenca Miocena Alto Tunuyán mediante petrografía y edades U-Pb LA-ICPMS de circones.

Análisis estructural y tectónico de la evolución de los Andes Centrales Australes.

Análisis de procedencia de sedimentos y evolución tectónica de la cuenca Alto Tunuyán.

Provincia de Cobre Andina: entornos tectonomagmáticos, tipos de depósitos, metalogenia y exploración.

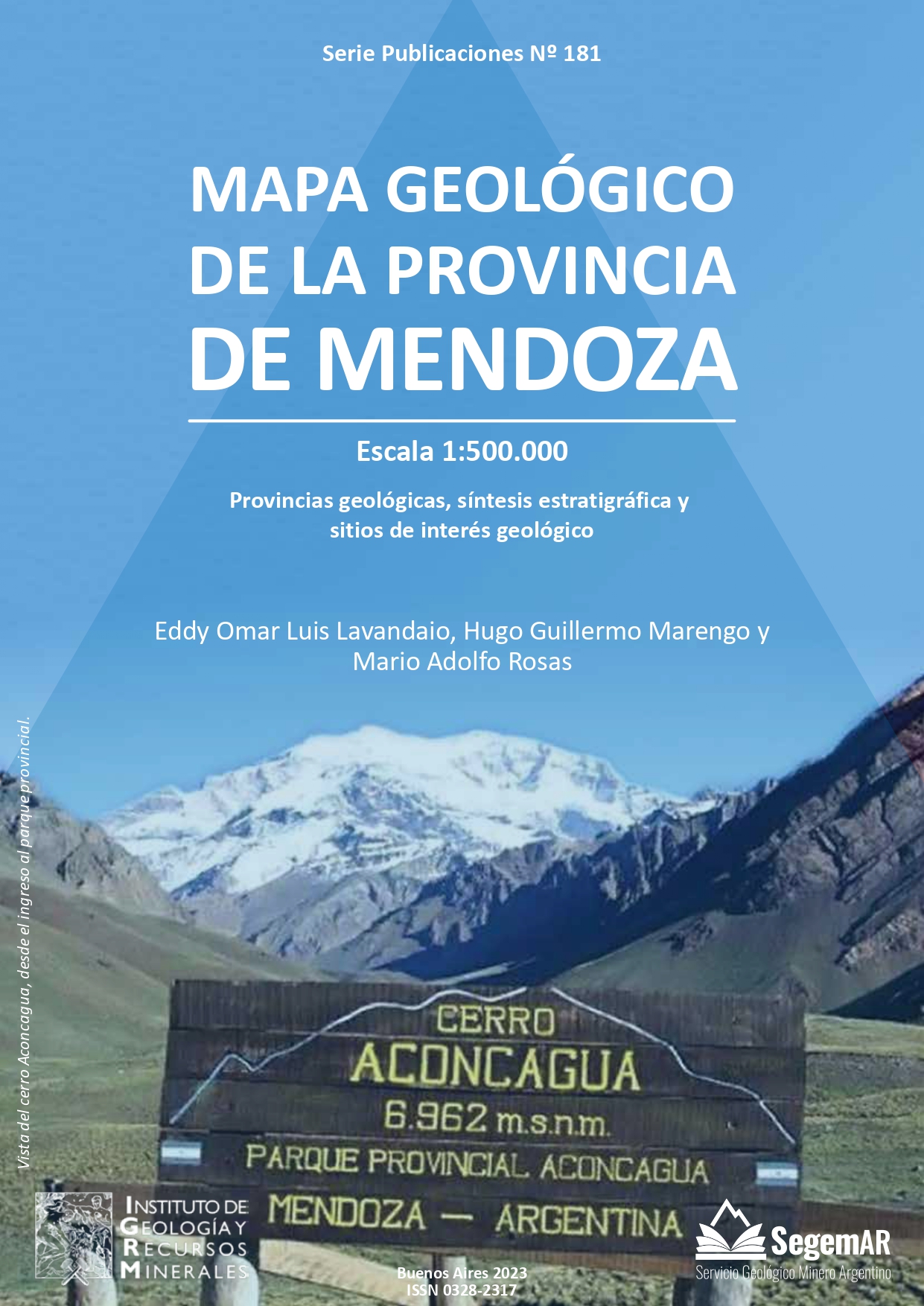

Serie Publicaciones N° 181, recursos de cartografía geológica y mineral para el sector Tunuyán a latitud 33°40′S.

Controles tectónicos sobre la deformación andina en la región del Alto Tunuyán.

Evolución estructural de los Andes en latitud 33°40′S, zona del Alto Tunuyán.

Inventario de glaciares y ambiente periglacial de la subcuenca del Río Tunuyán Norte.

Sección estructural esquemática del cinturón de plegamiento y corrimiento Aconcagua y Alto Tunuyán.

Patrones de deformación del foreland andino y sistemas estructurales.

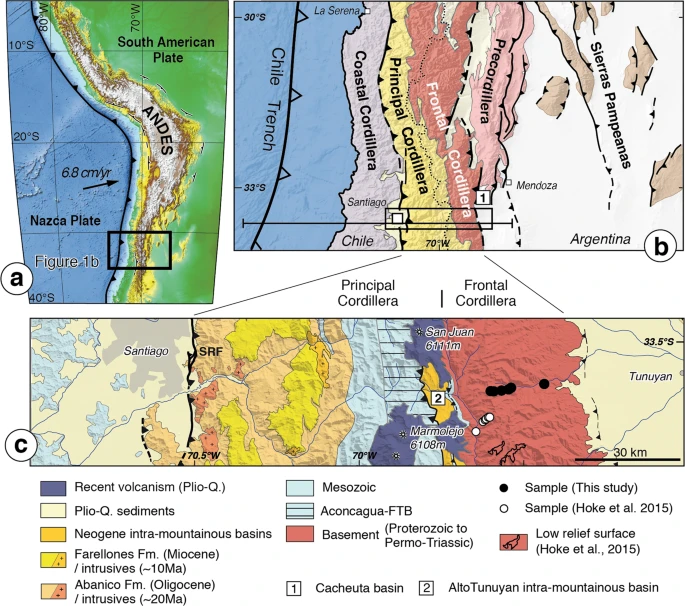

Divisoria de aguas Chile-Argentina con indicación del Paso Piuquenes y Alto Tunuyán.

Evolución de estructuras superficiales y profundas a lo largo del transecto Maipo-Tunuyán 33°40′S.

Estudio de sistemas de óxido de hierro cobre oro en ambientes de foreland fracturados de los Andes.

Controles estructurales y pulsos de levantamiento tectónico durante la Orogenia Andina en el Mioceno tardío.

Identificación y caracterización de núcleos de alteración potásica en sistemas de pórfido cuprífero.

Estudio del Complejo Campanorco mediante espectrometría de rayos gamma y series calc-alcalinas de alto potasio.

Modelos de alteración hidrotermal en estratovolcanes del Mioceno de la cordillera andina.

Análisis de testigos de perforación en áreas glaciadas de los Andes Centrales.

Sistemas de falla de tendencia noroeste y elementos guía cobre-hierro en los Andes Centrales.

Procesos hidroquímicos y niveles de fondo naturales en aguas subterráneas de Mendoza.

Uso del arsénico como elemento guía para la identificación de depósitos de sulfuros hidrotermales.

Caracterización geofísica de sistemas hidrotermales en la provincia de Mendoza.

Boletín N° 346, estudio geológico detallado del Cerro Tupungato y alrededores.

Boletín N° 252, estudio geológico de la hoja Mendoza y su contexto estructural.

Geolocalizador y Servicios Web del Servicio Geológico Minero Argentino.

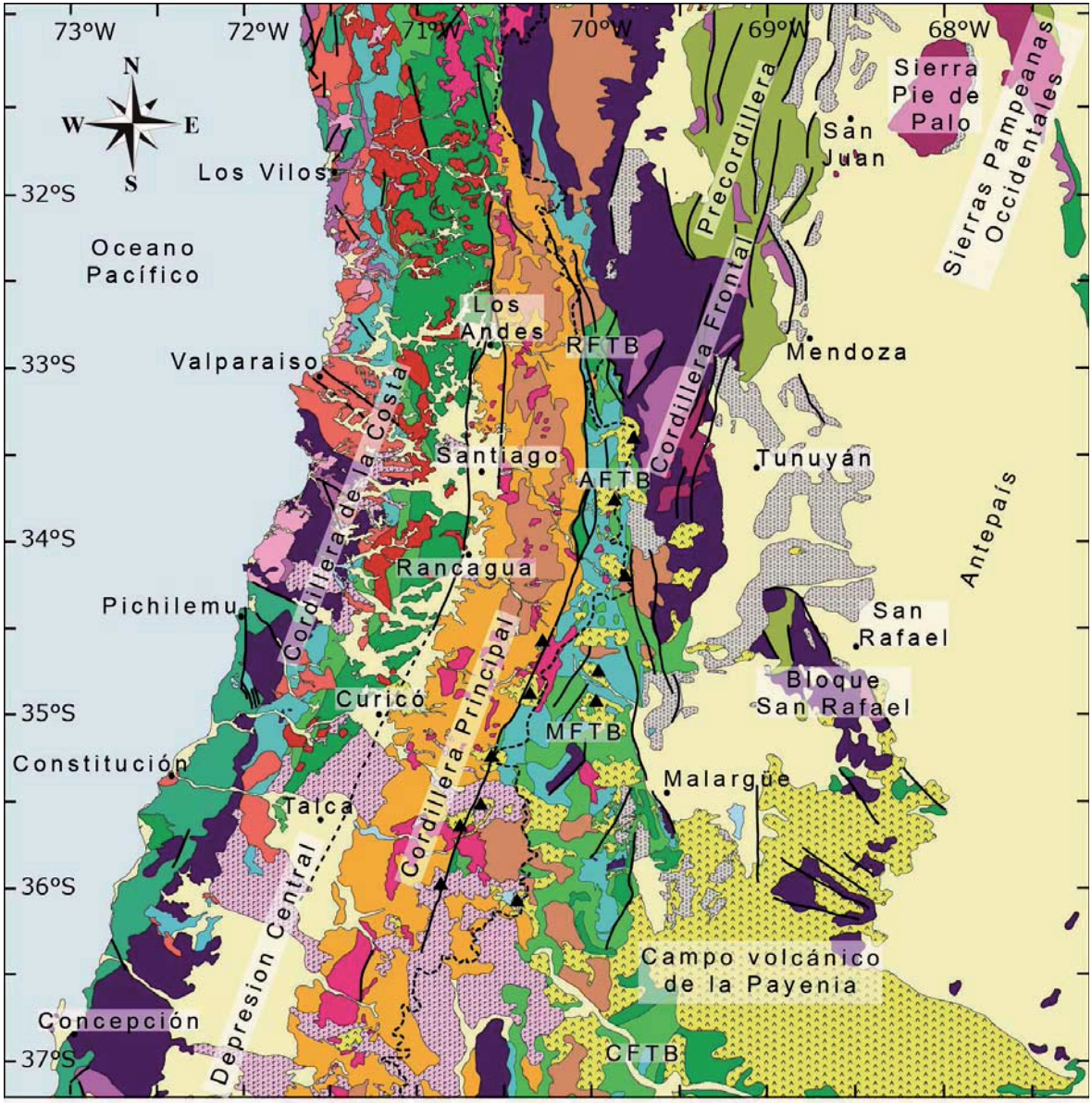

El mapa geológico sitúa a Alto Valle de Tunuyán en una zona de cruce entre corredores andinos históricos y fajas metalogénicas asociadas a cobre, hierro y potasio. Esta lectura refuerza el valor territorial del activo más allá del acceso binacional.

Los códigos del mapa corresponden a fajas metalogénicas: zonas geológicas definidas por la edad de las rocas y por la cordillera a la que pertenecen. En Mendoza, estas fajas permiten interpretar qué tipos de sistemas minerales podrían desarrollarse en cada tramo del corredor.

La región se relaciona con uno de los grandes distritos potásicos andinos. El potasio mantiene relevancia estructural para fertilizantes, seguridad alimentaria y cadenas de suministro agrícolas.

Los sistemas tipo skarn presentes en esta franja de la cordillera sugieren potencial para mineralización ferrífera asociada a intrusivos y reemplazo metasomático.

Las fajas miocenas son las más estratégicas para pórfidos cupríferos. El cobre sigue siendo el metal central de electrificación, redes, movilidad eléctrica y transición energética.

En síntesis: Alto Valle de Tunuyán se presenta como una encrucijada geológica donde se superponen corredores andinos históricos con cinturones favorables para minerales estratégicos de la economía industrial y energética contemporánea.

Nuestro territorio incluye 3 volcanes, 3 glaciares y múltiples sistemas de agua termal ricos en minerales. Esta convergencia geológica representa un potencial minero y geotérmico significativo.

Las aguas termales ricas en azufre (sulfuro) y hierro (ferroso) son fuertes indicadores geológicos de mineralización subsuperficial.

Las aguas hidrotermales disuelven y transportan metales desde profundidad hacia zonas superficiales.

Presencia potencial de cobre, zinc, plomo, plata y oro.

Travertino y costras minerales pueden contener concentraciones de valor económico.

Conclusión: La coexistencia de volcanes, glaciares, sistemas de azufre y aguas hidrotermales ferrosas representa una zona geológica de alto potencial para exploración mineral. Se requiere evaluación técnica integral para confirmar viabilidad comercial y asegurar desarrollo responsable de recursos.

Conclusión: La coexistencia de volcanes, glaciares, sistemas de azufre y aguas hidrotermales ferrosas representa una zona geológica de alto potencial para exploración mineral. Se requiere evaluación técnica integral para confirmar viabilidad comercial y asegurar desarrollo responsable de recursos.

Dentro de la tesis de inversión, la “profundidad óptima para la formación de pórfidos” se refiere a la ventana cortical donde los grandes sistemas de cobre tienden a formarse, estabilizarse y conservar relevancia para la exploración moderna.

Los depósitos de cobre tipo pórfido suelen formarse entre 1 km y 6 km por debajo de la paleosuperficie terrestre. Ese rango de profundidad refleja las condiciones de presión y temperatura necesarias para que los fluidos hidrotermales concentren cobre, molibdeno, oro y plata.

La propiedad Alto Valle de Tunuyán se ubica hoy entre 2.500 y 4.500 metros sobre el nivel del mar. Debido al levantamiento andino de largo plazo, esas elevaciones actuales corresponden a niveles corticales que originalmente estuvieron varios kilómetros por debajo de la superficie durante el Mioceno.

En términos geológicos prácticos, el levantamiento ha expuesto los niveles estructurales donde los sistemas porfiríticos fueron emplazados originalmente, comparables con los niveles exhumados observados en grandes distritos andinos como El Teniente.

El levantamiento andino pudo haber acercado de manera material la profundidad original de formación mineralizada a la superficie actual, aumentando la posibilidad de que un núcleo porfirítico hoy se encuentre dentro de profundidades accesibles por perforación.

Análisis estratigráfico, mineralógico y referencias institucionales

The Alto Valle de Tunuyán is characterized by its strategic location between the Principal and Frontal Cordilleras. The presence of Miocene volcanic rocks, large-scale structural lineaments, and specific magmatic suites provides a strong technical basis for copper (Cu), iron (Fe), and potassium (K) exploration.

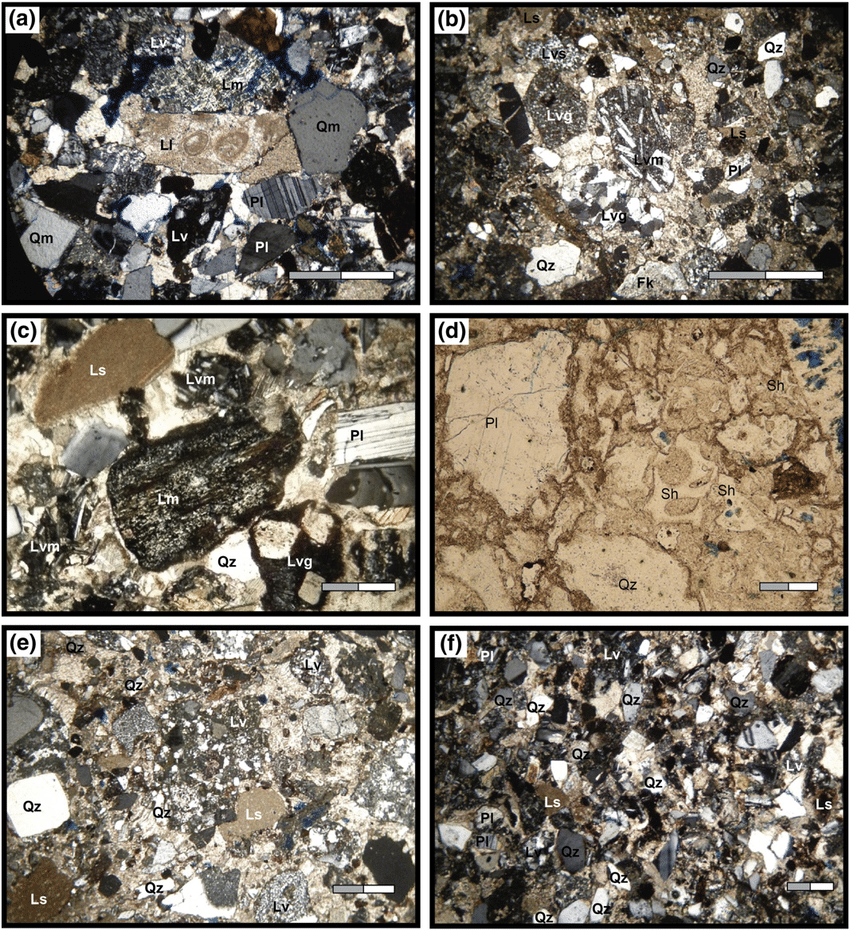

Generalized Stratigraphic Column: Petrographic analysis and U–Pb LA–ICPMS zircon ages indicate complex lithic compositions within the ~300 m thick Miocene Alto Tunuyán Basin sequence, which includes the Tunuyán Conglomerate and Palomares Formation [15]. The studies show a transition from lithoarenites to feldspathic lithoarenites, reflecting significant, coetaneous volcanic activity [16].

Source: Porras et al. (2016) - ResearchGate stratigraphic analysis of Alto Tunuyán Basin

Selected photos of sandstones from the Alto Tunuyán Basin. Detailed petrographic analysis reveals complex lithic compositions with various rock fragments, volcanic components, and mineral associations that provide insights into the sedimentary provenance and volcanic activity during the Miocene period.

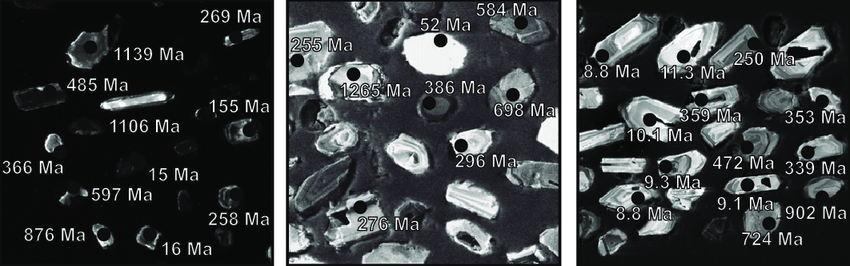

Figure 1: Petrographic thin sections showing lithic arenite textures

Figure 2: Cathodoluminescence (CL) images for zircons

Representative cathodoluminescence (CL) images for zircons of samples from the Alto Tunuyán Basin (CM2, CM5 and I2). Some analytical spot and 238 U/ 206 Pb ages are marked, providing crucial geochronological data for understanding the timing of volcanic activity and sediment deposition.

U-Pb zircon ages indicate Miocene volcanic sources

CL imaging shows complex zonation patterns

Analytical spots provide precise age constraints

Institutional Framework: The stratigraphic studies are complemented by comprehensive SEGEMAR geological mapping resources covering the Tunuyán sector at 33°40′S latitude [17].

The Miocene Alto Tunuyán Basin sequence identified by Porras et al. (2016) correlates with SEGEMAR's Farellones Formation mapping in Hoja 3369-II and 3369-III, providing integrated stratigraphic and structural frameworks for mineral exploration targeting.

Miocene Alto Tunuyán Basin and Farellones Formation sediment supply studies

IOCG systems in broken foreland settings of Central Andes

Andean Orogeny uplift pulses and structural controls on mineralization

Potassic alteration cores as primary hosts for copper mineralization

Gamma-ray spectrometry detection of K enrichments in calc-alkaline series

Property size and strategic location advantages

Binational access and infrastructure development potential

Proximity to Tier-1 copper districts and geological similarities

Choiyoi Group volcanics and associated mineral potential

Farellones Formation volcanic sequence and metallogenic significance

Major fault systems as fluid conduits for mineralization

Propylitic and argillic alteration mapping in Andean cordillera

Potassium anomalies and gold mineralization in San Rafael Block

Thermal springs and ferruginous waters as surface expressions of sulfide oxidation

Porras et al. (2016): Petrographic analysis and U-Pb LA-ICPMS zircon ages of Alto Tunuyán Basin sequence

Transition from lithoarenites to feldspathic lithoarenites reflecting coetaneous volcanic activity

SEGEMAR (2023): Geological and mineral mapping resources for Tunuyán sector at 33°40′S latitude

González Díaz, E.F. (2000): Hoja Geológica 3369-II "Mendoza", Boletín N° 252, SEGEMAR

Cortés, J.M. & González, R. (2005): Hoja Geológica 3369-III "Cerro Tupungato", Boletín N° 346, SEGEMAR

SEGEMAR (2023): Mapa Geológico de la Provincia de Mendoza, Serie Publicaciones N° 1822

SEGEMAR (2026): SIGAM Platform - Interactive GIS viewer, Geolocalizador, and Web Services

La Cordillera del Límite de Mendoza forma parte del sistema magmático mioceno responsable de los principales depósitos porfiríticos del lado chileno. La continuidad estructural y metalogénica sustenta el interés exploratorio del corredor.

Simple. Profesional. Tranquilo.

Hasta 10 zonas superficiales definidas disponibles para solicitud de permiso (≤10 Ha cada una). Cada cateo hereda la continuidad geológica, las tendencias estructurales y la lógica de exploración de su bloque de tierra padre.

View the complete plot plan and available inventory in real-time.

Structured surface access for exploration within the Andean Copper Belt at the same latitude as major copper deposits.

El Gobierno de Mendoza promueve activamente la inversión en minería, energía y petróleo como pilares estratégicos del desarrollo provincial. Bajo el liderazgo del Gobernador Alfredo Cornejo, Mendoza se posiciona como una jurisdicción confiable, fiscalmente responsable y legalmente segura para el despliegue de capital a largo plazo.

Con respaldo legislativo para proyectos de exploración y explotación, reformas para agilizar la obtención de permisos y un sólido marco institucional, Mendoza está lista para cooperar con inversores internacionales y brindar apoyo en cada etapa del desarrollo de proyectos.

The Mendoza Ministry of Energy and Environment, led by Jimena Latorre, is advancing a new mining district in Las Heras. Geological studies for the project, located near the San Jorge area, were confirmed during the PDAC mining convention in Canada.

President Javier Milei has placed large-scale foreign investment at the center of Argentina’s economic strategy, highlighting mining, energy, and strategic exports as pillars of growth. Through regulatory reforms and international engagement, the federal government seeks to attract and protect long-term capital in Argentina.

20 artículos de fuentes principales

Las revisiones de Javier Milei a la ley abrirán áreas de alta altitud a la minería y pondrán en riesgo las reservas de agua ya tensionadas por la crisis climática, dicen activistas

El fin del mito de la minería lenta: San Juan descubre yacimientos de cobre extraordinarios.

El experto en minería Roberto Cacciola destacó la necesidad de avanzar con proyectos concretos.

El proyecto Don Luis avanza con su Declaración de Impacto Ambiental en Mendoza.

Los Andes en Chile destaca la visión de Jimena Latorre sobre el rol de la minería.

El proyecto Los Azules tiene el potencial de convertirse en un importante productor mundial de cobre.

El sector minero mendocino se prepara para un crecimiento significativo en los próximos años.

Mendoza presentó en Canadá el proyecto de distrito minero en Las Heras.

La secretaria de Minería destacó los resultados positivos obtenidos en la feria PDAC de Toronto.

Jimena Latorre destacó la importancia de la minería al presentar Mendoza ante inversores en PDAC.

Mendoza se posiciona como destino atractivo para la exploración minera internacional.

Vicuña Corp confirma su compromiso de inversión histórica en proyectos mineros argentinos.

El presidente Milei recibió al CEO de Vicuña para anunciar una inversión récord en el sector minero argentino.

Embajador canadiense destaca el creciente interés de empresas de Canadá en la minería argentina.

Proyectan inversiones por u$s63.700 millones y exportaciones que podrían quintuplicarse hacia 2035.

La justicia argentina rechaza el pedido de Barrick contra la ley de protección de glaciares.

El gobierno argentino impulsa cambios en la ley de glaciares para facilitar proyectos mineros.

Lundin Mining anuncia que Vicuña Corp presentó solicitud para el régimen RIGI.

La Cancillería argentina publica guía completa sobre el RIGI para grandes inversiones mineras.

Alfredo Cornejo expuso ante empresarios en Londres las oportunidades de inversión en Mendoza.

RIGI offers 30 years of tax stability, zero export duties, and full FX freedom for qualifying Tier-1 copper–gold projects. Our asset qualifies — here's why it matters for your portfolio.

Guaranteed protection against tax increases or regulatory shifts, essential for long-life copper and gold assets.

After the third year of operation, all mineral exports are exempt from duties, maximizing international competitiveness.

Full exemption from import duties on specialized mining machinery and spare parts to fast-track construction phases.

Direct access to international currency markets and 100% exemption from local settlement requirements for export proceeds by year four.

Applications are being processed through July 2026. Contact us to understand the full financial impact of RIGI on project economics and investor returns.

We operate within Argentina's strict environmental framework. No cyanide. No glacier destruction. No water contamination. No water wasting. This is non-negotiable.

Compliant with Mendoza Law 7722. All processing via flotation concentrate (no leaching). Copper recovery without toxic reagents.

Full compliance with National Glacier Law 26.639. No operations within 1km of glacier boundaries. Continuous satellite monitoring.

Closed-circuit water systems mandatory. Zero discharge to the Rivers. All process water recycled (>95% recovery rate).

Geothermal energy from Tupungatito volcano powers operations. Eliminates diesel dependency and reduces water consumption by 70%.

La propiedad incluye nacientes asociadas con los ríos Tunuyán, Palomares y Las Tunas.

El concepto del proyecto prioriza el cumplimiento regulatorio y la gestión ambiental consistente con el marco procedimental minero actualizado de Mendoza.

Se requieren estudios geológicos, ambientales e hidrológicos independientes previos al desarrollo.

El Alto Valle de Tunuyán ha estado en posesión de nuestra familia desde 1822. Este suelo es el legado de los hermanos Lemos, quienes como Libertadores del Ejército de los Andes, sirvieron junto al Libertador José de San Martín para forjar la independencia de Sudamérica.

Para consultas sobre acuerdos de acceso superficial cateo y coordinación de exploración.

La información presentada en este sitio web es de carácter general e informativo. No constituye una oferta de venta, una solicitud de oferta de compra, ni una recomendación de ningún valor, producto de inversión, transacción o estrategia de inversión.

Los indicadores geofísicos preliminares sugieren potencial porfirítico. No se ha realizado perforación ni estudios formales para confirmar la mineralización. Se requiere verificación técnica independiente antes de cualquier decisión de inversión.

Las estructuras de participación descritas son indicativas y están sujetas a negociación, debida diligencia y cumplimiento con las leyes argentinas aplicables.

El proyecto cumple con la Ley 7722 de Mendoza (prohibición de uso de cianuro), la Ley Nacional de Glaciares 26.639 y los requisitos de sistemas de circuito cerrado de agua.